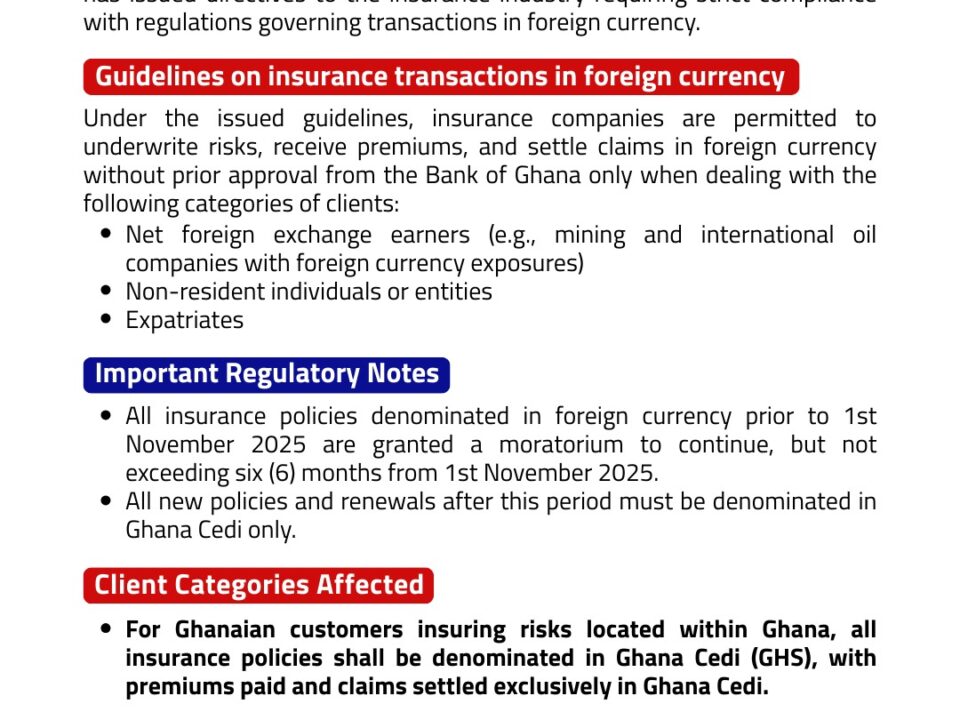

Change Has Indeed Come: The New Law and the Player

CHANGE HAS INDEED COME: THE NEW LAW AND THE PLAYER

The Player

Do you want to set up an insurance entity? Have you gone through the licensing process? Are you left endlessly second-guessing, wondering ‘he loves me; he loves me not’, as a response from the Commission is taking forever to get to you? Well, those days are, with this new law, the Insurance Act, 2021 (Act 1061), over. Because section 44 of the Act directs the Commission to notify you in writing if your application has been rejected, or if there are any conditions imposed by the Commission requiring your performance before such licence will be granted you. The Commission is by law directed to go a step further to provide you reasons for this refusal or imposition of conditions—all of this done within 14 days after the Commission has made its decision. And where the application for licence has been granted, notification of your status shall be made you, and a publication to its effect done in the Gazette and on the website of the Commission.

For industry players like insurance and reinsurance companies, intermediaries such as insurance and reinsurance brokers, etc. to be able to effectively play their role of, among others, driving insurance penetration and economic integration, undertaking prompt claim settlements etc., these entities must have robust systems of governances in place—systems that ensure their most optimum functioning and performance as body corporates. Thus, the new law seeks to improve corporate governance of insurance entities, ensure compliance with laws and regulations as locally enacted. In this highly globalised world, nations do not exist in isolation. Hence not only are countries’ institutions and systems expected to satisfy local expectations and needs; they must go a step further to comply with international best practices. These, among many others, are the philosophical underpinning behind the new insurance law. Section 84 sums this up by providing for a set of core values, ‘obligations for conduct of business’ that insurance entities are to be guided by—principles of, among others, integrity, optimum skill, due diligence, care.

And to ensure a healthy insurance market, insurance entities operating within the industry must be healthy. In new provisions like sections 54 and 124 the Commission is given a supervisory eye and an influential say over the ownership structures and interest holdings of insurance companies and intermediaries respectively. Before a person may become a significant owner of an insurance and reinsurance entity and intermediary firm, or before they can significantly increase their level of control over such entities, they must have sought and received the written approval of the Commission. The flouting of this provision gives the Commission the power to demand the disposal of such interests or prohibit the exercising of this rights of ownership or control, as stipulated in sections 54 and 124. The same goes for persons who the Commission has ground to believe does not fit or meet the proper requirements spelt out by law.

In sections 56 and 126 we see a similar power granted the Commission once again, this time around, regarding directors and key persons managing insurance companies and intermediaries respectively. The Commission is with this section, empowered to demand the removal or replacement of directors and persons in positions of power within an organisation, such as senior managers, persons in key control functions, etc., when it has reason to believe that such persons are not “fit and proper” for the job.

Sections 78 and 135 provide for the putting into place, risk management strategies by insurance entities. In section 62, every “long-term insurer or reinsurer” is required to establish and maintain segregated funds. On the matter of reinsurance, sections 72 and 73 provide for licensed insurers and reinsurers to establish and maintain written retrocession/reinsurance strategies and written reinsurance procedure, and must see to their implementations. Strategies must take into consideration the nature, scale, complexity and diversity of the business, risk profile, and risk tolerance of that insurer or reinsurer, all the while complying with the Commission’s directives on the matter.

Section 99 provides for the appointment of statutory management by the Commission to “prevent or limit the impact of the risk of failure of a licensed insurer or reinsurer.” Section 167 makes provision for the Commission to direct insurers and reinsurers who are distressed to prepare and submit a ‘Recovery Plan’—that is if the Commission has reason to believe, among others, that such insurer or reinsurer has breached, is breaching, or is likely to breach a solvency control level; or if they have not conducted their business in a prudent manner or in accordance with sound insurance principles, etc.

A person who is believed to have information relevant to the Commission in the performance of its duties may by a notice in writing be called on by the Commission to answer relevant questions—and this is according to section 172 of the Act. Per section 176, the Commission has the power to appoint “persons with relevant competence as investigators to conduct investigations [into insurance entities] on behalf of the Commission.”

The Endgame

Any insurance market is, as noted, only as good as the insurance entities contained within it. Many an insurance industry worldwide face threats of decline due to how poorly their insurance entities are regulated. A poorly regulated insurance market means a poorly serviced insurance market. Low to no legitimate claim pay-outs become the order of the day if the law does not undertake effective and sustained supervisions of all aspects of the operations of insurance entities—right from their governance, to their operations, to the insurance products and services they put on the market, to arguably the most important ingredient of them all, how quickly and efficiently they are to pay legitimate claims.

And this is precisely the endgame of this new insurance law: that Ghana’s insurance story be a successful one, not one headed for a decline.

[By Kafui. Research & Development.]

{kind=link}

{kind=link}

{kind=link}